Economic events scheduled for today

02:30 AUD CPI (QoQ) 0.6%

The Consumer Price Index (CPI) measures the change in the price of goods and services from the perspective of the consumer. It is a key way to measure changes in purchasing trends and inflation.

07:00 EUR Finnish Unemployment Rate 7.40%

The unemployment rate represents the number of unemployed persons expressed as a percentage of the labor force. The unemployment rate for a particular age/sex group is the number of unemployed in that group expressed as a percentage of the labor force for that group.

10:00 EUR Industrial New Orders (MoM) -0.5% -2.3%

Industrial New Orders measures the change in the total value of new purchase orders placed with manufacturers. It is a leading indicator of production. A higher than expected reading should be taken as positive/bullish for the EUR, while a lower than expected reading should be taken as negative/bearish for the EUR.

13:30 CAD Retail Sales (MoM) 0.5%

Retail Sales measure the change in the total value of inflation-adjusted sales at the retail level. It is the foremost indicator of consumer spending, which accounts for the majority of overall economic activity. A higher than expected reading should be taken as positive/bullish for the CAD, while a lower than expected reading should be taken as negative/bearish for the CAD.

15:00 USD CB Consumer Confidence 70.3 70.8

Conference Board (CB) Consumer Confidence measures the level of consumer confidence in economic activity. It is a leading indicator as it can predict consumer spending, which plays a major role in overall economic activity. Higher readings point to higher consumer optimism.

15:00 USD New Home Sales 320K 313K

New Home Sales measures the annualized number of new single-family homes that were sold during the previous month. This report tends to have more impact when it’s released ahead of Existing Home Sales because the reports are tightly correlated

Euro Dollar

EURUSD (1.31.54) EUR is weak leading into the North American session, having lost 0.2% since Friday’s close, but still trading within Friday’s range. After several economic indicators have surprised higher over the last week, today’s release of PMIs were disappointing.

The Eurozone composite fell to 47.4 (consensus was 49.3, while March’s was at 49.1), the weakness was in both manufacturing and services; with the most concerning surprise coming from German manufacturing which fell to 46.3 (well below the 50 expansionary territory); while France disappointed on services, which fell to 46.4. Also weighing on the currency is news that the Netherlands have failed to reach an agreement on austerity, resulting in what will likely be early elections.

Finally, in the first round of French elections Francois Hollande won 28.6% of the vote, while Sarkozy won 27.1%, leaving the two in a face‐off for the May 6th second round election. A Hollande victory, which is widely expected, is likely to be mixed for markets. On the negative side, he would like to re‐open discussions on the fiscal pact, cancel the VAT and impose a 75% tax rate on those who earn more than €1m; however his policies are far more favorable towards growth than President Sarkozy, which in the current environment would be encouraging for markets.

The Sterling Pound

GBPUSD (1.6114) Sterling sparkled during last week’s session, out-performing nearly all of the other sixteen most-actively traded global currencies, following a string of encouraging data releases. With numbers released earlier in the week confirming that the level of domestic unemployment was on the wane and that last month had seen an unexpected uptick in inflation, Friday’s UK Retail Sales data for March, which thrashed expectations to print at 3.3%, made sure that the Pound ended the week with a bank. Analysts had been expecting an increase of only 1.3% in British shop in March. The unexpectedly strong showing was attributed to unseasonably hot weather in the UK last month, and to panic buying of petrol supplies by British drivers due to fears of a tanker driver strike.

The positive week of UK data saw the Pound climb to significant levels against several other major currencies, with GBP EUR breaking to a new 20-month high of 1.2252 on Thursday. Meanwhile, Sterling jumped to 1.6150 against the US Dollar on Friday – a level which has not previously been seen since October of last year.

As this week’s session gets underway, the Pound appears to be losing its luster a little; last night saw both the GBP EUR and GBP USD exchange rates open at a lower level than their Friday close. A downward ‘price gap’ is most often considered a negative indicator by technical analysts, so the portents do not appear good for the chances of another strong week for the Pound. With Wednesday’s initial UK GDP Q1 growth numbers expected to show a slight expansion in British economic activity of 0.1% in the first three months of 2012, there appears to be pronounced danger of Sterling weakness. If the key figure shows at anything less than the expected level, then the UK economy will have registered two consecutive quarters of non-positive growth and Britain will officially have slipped back into recession.

Asian –Pacific Currency

USDJPY (81.52) JPY is strong having gained 0.6% since Friday’s close, on the back of risk aversion; however the currency is likely to come under renewed pressure as we move towards this week’s BoJ meeting (April 26/27). Leading into the decision, March CPI is expected to climb to 0.4%y/y on headline and fall 0.5% ex food and energy; leaving inflationary pressures in Japan a long way from the BoJ’s target of 1%. Accordingly for the BoJ to maintain its credibility it needs to act fairly aggressively to bring inflationary pressures back into the system. The BoJ rate decision is likely to see the central bank announce yet another round of asset purchases. Such a dovish stance will weigh on the currency; as long as the FOMC decision on Wednesday is as expected.

Accordingly, we would expect USDJPY to test back up towards 82.00 over the next few sessions.

Gold

Gold (1638.03) Gold fell in the early part of the US session but is has picked up some of the loss as investors position themselves before Tuesdays FOMC meeting. Business activity across the 17-nation euro zone contracted at a faster-than-expected pace in April, according to the preliminary purchasing managers’ index, or PMI, readings released Monday by data firm Markit. Manufacturing PMI fell to 46.0

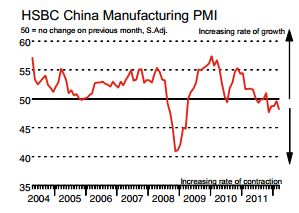

Business conditions in China improve for manufacturers in April from levels seen in the previous month, although activity in the sector continues to decline, data released by HSBC show, prompting calls for Beijing to loosen its policies.

Crude Oil

Crude Oil (102.91) edged lower on Monday on pressure from revived concerns about a euro zone economic slump and political uncertainty, while a North Sea production problem and worries about Iran and potential supply disruptions limited losses. Euro zone business contraction deepened at a faster pace than expected in April, with the Purchasing Managers Index for the bloc’s dominant service sector falling to a five-month low, against forecasts that it rose, Reuters reported.

The signs of euro-zone economic and political turmoil sparked a “risk-off” trade, pushing global equities, the euro and key industrial feedstock copper lower and sending investors in the direction of perceived safe-haven assets such as the dollar and US Treasuries, the news wire said.