Euro Dollar

Today, the calendar is thin. In Europe, the Spanish Parliament will discuss the new 2012 budget. This might cause some euro negative headlines and analysis on the country. However, the situation of Spain is already well documented. So, the impact on EUR/USD trading might be limited. In the US, the factory orders will be published. A decent figure might be moderately supportive for risk taking.

Usually, the report is only of intraday relevance for global markets and for EUR/USD trading. So, we can expect more erratic trading in holiday thinned market conditions. In a day-to-day perspective we expect EUR/USD to stay near current levels. Later in the session, the minutes of the previous Fed meeting are a wildcard. Markets will look whether there is any change in the balance for more QE. If some members would turn more cautious on the option of more QE, this might be USD supportive.

EUR/USD reached a reaction low at 1.2624 after the S&P downgrade of several EMU countries. From there, a technical rebound kicked in. EUR/USD reached a top for this year at 1.3487 late February. However, there were no follow-through gains and EUR/USD returned soon in the previous consolidation pattern. Mid March, global dollar strength brought EUR/USD within striking distance off the 1.2974 ST range bottom. The euro is now trading toward the higher side of the range, more due to the emergency measures of the EU and ECB, now that this is behind us the euro should find its true value, which could be under the 1.32 range.

The Sterling Pound

On Monday, sterling had a good run both against the euro and to a lesser extent also against the dollar. Technical considerations played a role, but the UK currency was also supported by a better than expected PMI of the manufacturing sector. EUR/GBP hovered in the 0.8340 area in Asia. However, the UK currency fund a better bid from the start of trading in Europe.

The momentum on the UK currency improved further after the publication of a better than expected UK PMI of the manufacturing sector. The pair drifted lower for most of the European trading session and reached an intraday low just below the 0.83 mark late in Europe. From there, the pair regained some ground in lockstep with the rebound of the EUR/USD headline pair.

EUR/GBP closed the session at 0.8313, compared to 0.8327 on Friday evening. So, sterling succeeded a good intraday performance, but in a broader perspective, EUR/GBP still holds perfectly within the sideways consolidation pattern.

Today, the construction PMI will be published. This indicator is usually not that important for sterling trading. The consensus is looking for a decline from 54.3 to 53.4. Another positive surprise after the yesterday’s manufacturing measure might sustain the ST sterling positive mood, especially in current thin market conditions. Late last year and early this year, the EUR/GBP cross rate joined the broader market repositioning out of the euro.

Investors were well aware that the ECB will keep monetary policy extremely loose in the foreseeable future and that the ECB would continue to provide ample liquidity. The poor eco outlook and the unresolved debt crisis caused the euro to lose its advantage over the UK currency. Finally, the downside was blocked, as the 0.8222 support held and several other key support levels are lining up (0.8142/0.8068). On the topside, the range top in the 0.8400/22 area was tested several times, but a break didn’t occur until late February.

This break improved temporary the ST picture in this cross rate. However, there were no follow-through gains and the pair returned soon in the old sideways range. For now we don’t see a trigger for the pair to leave the 0.8222/0.8424 consolidation pattern. Within this range, we still slightly prefer a sell-on-upticks approach.

Asian –Pacific Currency

Yesterday, USD/JPY remained under pressure throughout the whole day. The rather poor Tankan survey had only a limited (negative) impact on the yen even as there was a lot of market talk on more BOJ stimulus in the (near) future. Later in the session, cautious sentiment on risk and declining core bond yields caused USD/JPY give up more than 1 big figure. USD/JPY reached an intraday low at 81.88 late in Europe. Contrary to what happened in other market/cross rates, USD/JPY failed to profit from improving sentiment on risk. USD/JPY closed the session at 82.08, compared to 82.87 on Friday evening.

This morning, the profit taking move on Japanese equities and the liquidation of USD/JPY long positions continues. The recent decline in US bond yields clearly prompted profit taking in USD/JPY. So, USD/JPY traders will look out whether improving sentiment on risk or good US eco data are able to put a floor for US bond yields.

As long as this is not the case, the correction might continue. The pair is again testing the 81.98 neckline. Sustained trading below this level might suggest that the correction has some further to go. The 80.59/80.00 is the next point of reference on the charts.

Tomorrow brings us the OZ Trade Balance which measures the difference in value between imported and exported goods and services over the reported period. A positive number indicates that more goods and services were exported than imported. The current forecast is for 1.00B a complete reversal from the negative report last month.

The Australian dollar fell after Australia’s central bank decided to leave the cash rate on hold. The Reserve Bank of Australia has left the cash rate at 4.25 per cent after its April board meeting on Tuesday. The local currency was trading at 104.55 US cents just before the decision was announced, and fell to 104.15 US cents just after.

Retail sales in Australia rose less-than-expected last month, data showed today. In a report, Australian Bureau of Statistics said that Australian retail sales rose to a seasonally adjusted 0.2%, from 0.3% in the preceding month. Analysts had expected Australian retail sales to rise 0.3%

Gold

Gold jumped again in today’s session climbing +9.55 to 1681.45

The move was supported by strong ISM manufacturing data in the US and a surprising ISM report from India. Indian manufacturing activity slowed in March, mainly due to power outages and shortages of raw materials, according to HSBC’s monthly manufacturing survey. HSBC’s manufacturing purchasing index slowed to 54.7 in March from 56.6 in February.

Rumors are circulating that jewelers in India, one of the world’s largest gold markets are expected to reopen for business after a two-week strike provided further support. Analysts said the decision may revive demand in the world’s largest gold consumer in 2011.

The upward movement in dollar-denominated gold is also in reaction to slightly weaker U.S. dollar and, along with entering the new quarter.

Bank of America-Merrill Lynch Monday cuts its 2012 outlook for gold, while upgrading its outlook for industrial metals like copper. The bank cuts its gold forecast for this year by 5.4% to $1,750 a troy ounce from $1,850/oz previously.

Crude Oil

Crude Oil is trading at 104.67 up from 103.31 and several economic reports and on geopolitical rumors from southern Iraq. News came forward today that there is a possible supply disruption from the Kurdish territory in Iraq. The market is also finding support after the Kurdistan region of Iraq halted exports because of a dispute regarding payments with Baghdad.

The self-ruled Kurdish region announced the halt in oil exports late Sunday, attributing the halt to Baghdad’s failure to send payments since May, even though the region had been exporting 50,000 barrels per day, according to Associated Press.

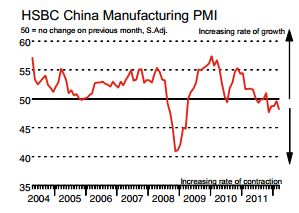

Also, China’s manufacturing got a mixed assessment on Sunday, as the official survey for March improved to its highest in a year and a competing survey by HSBC showed the sector moving deeper into contraction.