Global markets were in double jeopardy this week, with continuing weakening of economic fundamentals worldwide along with steadily falling gains from different asset classes. US markets made another toppled closing this week with sharp sell-off in the banking shares due to a huge trading losses posted by JP Morgan, however sell-offs was partly offset by strong buying in technology shares.

JP Morgan said it lost at least US$2bn from a failed hedging strategy and became the latest confidence-shaking bank on Wall Street to get waylaid by today’s financial system. However, the economic data were positive as US consumer sentiment rose to its highest level in more than four years in early May as Americans remained upbeat about the job market. The survey was a welcome sign amid worries that the economic recovery may be slowing down.

Among the major US indices, Dow Jones fell by 1.7%, followed by S&P 500 (-1.2%) and NASDAQ (-0.8%) fell over fear of market slides. On the European side, stocks declined for a second week after an inconclusive election in Greece left political parties struggling to form a government, increasing speculation that the nation might fail to implement austerity measures. Pressure on Spanish bonds abated, a day after the government moved to partly nationalize the country’s fourth-largest lender and was expected to take further action to shore up a financial sector decimated by the collapse of a property bubble

Euro Dollar

EURUSD (1.2914) The Euro remained under the significant 1.30 level against the U.S Dollar yesterday, as markets lacked the impetus to break out from narrow ranges. After failing to form a government, the SYRIZA coalition in Greece handed the baton over to Pasok who came third in the election last week. That just gives some indication over the political circus engulfing the nation and there is doubt whether any semblance of credible government can be formed.

There is still the obstacle that Greece does want to stay in the Euro, but not maintain the austerity program. ‘Have your cake and eat it’ springs to mind but the IMF led Troika will be reluctant to release financial aid to Greece if they don’t follow through on their commitment to austerity. Actions of the German government and the IMF will continue to be watched closely in the short-term.

The Sterling Pound

GBPUSD (1.6064) The Pound rallied to the strongest level against the Euro since November 2008 yesterday, while the UK currency also made gains versus the majority of the 16 most actively traded currencies, after the Bank of England elected not to increase quantitative easing this month, despite the UK economy suffering a double-dip recession.

UK government bonds fell as policy makers maintained asset purchases at £325 billion, while keeping the interest rate on hold at 0.5%. There was some speculation that the Central Bank could react to the recent growth figures by increasing stimulus measures to support the economy. That still remains a possibility if the recession is deeper than first anticipated but the Pound gained some relief following the announcement.

The UK currency has weakened against the higher-yielding currencies, amid a general improvement in global risk appetite.

Asian –Pacific Currency

USDJPY (79.92) This morning, global sentiment on risk has turned negative again, pushing USD/JPY back below the 80.00 mark. Risk sentiment and, to lesser extent, US bond yields and US eco data will remain the key factor for yen trading. For now, we don’t see a trigger for a sustained rebound of USD/JPY.

Gold

Gold (1579.25) Gold slid lower as a sharp drop in the Euro and ended at $1579 an ounce. The physical demand is seen emerging from Asia as traders and investors hunted the low price advantages. Demand owing to peak marriage season in India coupled with Chinese demand held the physical market firm. At the same time, European Union leaders meeting on May 23rd will be a short term focus.

Crude Oil

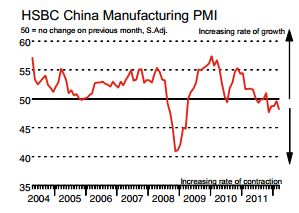

Crude Oil (95.65) Nymex crude oil prices continued taking cues from expectations that Europe’s debt crisis will worsen further coupled with rise US crude oil inventories which stood at its highest point in 22 years. Additionally, a stronger dollar index also acted as a negative factor for the crude oil. With lackluster data from China demand is seen dropping.