While investors initially cheered the plan to rescue Spanish banks, many details remain to be finalized, including how much money the banks will need.

European Union finance ministers agreed Saturday to lend up to €100 billion to the Spanish bailout fund to recapitalize insolvent banks. But the amount needed will not be known until an external audit of the banks is completed later this month.

It’s also unclear how the loans will impact the Spanish government’s credit rating, although the rescue will not involve any new austerity measures. Investors are on the lookout for another downgrade of Spanish debt after Fitch cut the nation’s credit rating to one step above junk status last week.

The deal was put together quickly as EU authorities hope to eliminate speculation about Spanish banks ahead of the elections in Greece.

Asian Stocks are in a decline today after Monday’s gains, as the elation over the Spanish banks getting a bailout took the backstage. The Greek polls and global slowdown is further pressuring stocks. The euro has also fallen below the 1.25$ mark, after rallying to two-month highs yesterday.

This effect is being felt in Asian currencies as well, as most of them declined early this morning. On the economic front, UK we have the Industrial production data from the UK, which is expected to increase to 0.10% from a previous reading of -0.30%, and could help the currency. From the US, the Import price index would be closely watched and could hurt the dollar with its decline this time around.

Euro Dollar:

EURUSD (1.2470) The euro was on the defensive on Tuesday as worries over Spain’s hurried bank bailout were compounded by jitters about upcoming elections that may determine Greece’s future in the euro.

Initial euphoria over Spain’s weekend deal quickly evaporated as investors feared the bailout-related payments could rank ahead of regular government debt in the queue for repayment, adding to its high borrowing costs.

There were also concerns that existing bondholders could sustain losses in any debt restructuring if the euro zone’s permanent bailout fund was used for the rescue.

These jitters saw the euro come off its Monday high at $1.2672 to last stand at $1.2470, still some distance away from the two-year low at $1.2288 hit earlier in the month.

The Great British Pound

GBPUSD (1.5545) Sterling rose against the dollar on Monday, tracking other riskier currencies on relief that Spain’s ailing banking sector secured external funding and pared losses against the euro, which had jumped to a near 1-1/2 month peak.

Traders said investors cut large bearish bets on the common currency but the bounce showed signs of waning on nervousness ahead of Greek parliamentary elections this weekend and as terms of the Spanish deal are still not clear. Many saw the bailout as a short-term fix which did little to change the euro’s bearish outlook in the near term.

Sterling was up 0.5 percent against the dollar at $1.5545, not far from a one-week high of $1.5601 struck on Thursday. It rose to a session high of $1.5582 with traders citing offers to sell above $1.5600.

Asian –Pacific Currency

USDJPY (79.32) Underscoring the prevailing bearish sentiment, bets against the euro surged to a record high in the latest week, while net long U.S. dollar positions extended gains, according to the Commodity Futures Trading Commission.

Against the yen, the euro fell 0.2 percent to 98.95 yen , with traders citing selling by model funds and Tokyo players dumping long positions in the pair.

Reflecting the brittle mood and the fall in the U.S. Treasury yields, the dollar dipped against the safe-haven yen to 79.32 yen, coming off the previous day’s high at 79.92 yen. The crucial support was seen at 77.65 yen hit on June 1.

Traders said any rise in the dollar may be curtailed by offers ahead of 80.00 yen. They added there are stop-loss orders above 80.00, and larger ones above 80.25 with the ascending 100-day moving average at 80.21 serving as a resistance.

The Australian dollar was last trading at $0.9875, from $0.9980 in late local trade on Monday. It rallied to $1.0010 early on Monday as short-covering kicked in after Spain’s rescue.

The Aussie now looks set to test minor support around $0.9820, with resistance sitting around $1.0010. Australia reopens after a public holiday on Monday.

Gold

Gold (1589.89) edged lower on Tuesday for the first time in two sessions but losses were limited because investors, who now doubt the effectiveness of the euro zone’s bailout plan for Spain’s banks, still believed in gold’s safe-haven status.

Spot gold lost 0.3 percent to $1,589.89 an ounce.

U.S. gold futures contract for August delivery also inched down 0.3 percent, to $1,591.40.

The initial euphoria in the financial market over the euro zone’s decision to shore up Spain’s banking sector quickly fizzled, as investors worried about the bailout’s impact on public debt.

Riskier assets, including equities, base metals and oil, slid as the market sentiment soured, outpacing losses in precious metals.

Crude Oil

Crude Oil (82.70) fell yesterday on the realization that a short-term fix in Spain won’t offer a long-term solution to Europe’s debt crisis Benchmark oil fell US$1.40 to US$82.70 per barrel in New York. Brent crude, which is used to price international varieties of oil, dropped 81 cents to US$98.66 per barrel in London. The broad S&P 500 stock index fell nearly one per cent.

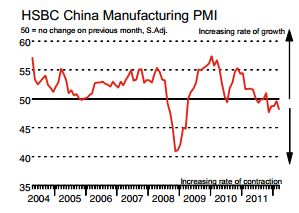

Oil jumped above US$86 per barrel in trading in Asia. But the relief was temporary, replaced by concern over Spain’s ability to repay the money. The potential for Greece to abandon the European current still hangs over the market, as does a deepening recession in Italy. That turmoil, as well as slowing economic growth in China and the US, is reducing demand for oil, gasoline and diesel fuel.