The US markets ended mixed amid a slew of earnings news after moving mostly lower over the course of the three previous sessions.

The mixed performance on Wall Street came as traders digested quarterly results from large companies, with disappointing news from Apple offset by upbeat results from companies such as Caterpillar and Boeing. Further, a report showed an unexpected drop in new home sales in of June. The Dow climbed 58.7 points or 0.5% to 12,676.1 while the Nasdaq fell 8.8 points or 0.3% to 2,854.2. The S&P 500 closed nearly flat, edging down 0.4 points to 1,337.9.

Markets were more focused on UK GDP results and Spain, Greece and Italy’s on going debt crisis.

With the Olympics beginning tomorrow and the month end data not due until early next week the currency and equities markets are expected to be fairly quiet.

Euro Dollar:

EURUSD (1.2150) The euro rose for the first time against the dollar in six days on Wednesday after a European Central Bank member said he could see grounds for giving the euro zone bailout fund a banking license that would increase its crisis fighting firepower. The comments from Ewald Nowotny prompted a flurry of short-covering and helped the euro rebound from a two-year low as investors who had bet against the single currency were squeezed out of those positions.

The Spanish 10-year government bond yield fell to roughly 7.40 percent on Wednesday, but is still at levels that are deemed as unsustainable, and is not far away from a euro era high of about 7.75 percent. The U.S. dollar briefly pared losses against the euro after data showing new U.S. single-family home sales in June fell by the most in more than a year dented risk appetite. But the impact was short-lived as the data fueled expectations of further stimulus from the Federal Reserve

The Great British Pound

GBPUSD (1.5479) The first cut at Q2 GDP figures for the UK came in at -0.7% q/q vs. -0.3%, way below the -0.2% expected (-0.8% y/y vs. -0.2%, expected -0.3%). Even though the CBI orders reading improved to -6 from -11 (expected -12), sterling suffered for much of the day.

Asian –Pacific Currency

USDJPY (78.13) No matter what the BoJ and the MoF say or threaten they seem unable to control the strength of the JPY. The pair continue to range trade below the 78.25 level.

Gold

Gold (1602.75) Gold opened a little higher at $1602.00 as the dollar remained the preferred safety trade. An early morning attempt toward higher levels as the EUR enjoyed a short lived mini rally saw gold reach a intraday high of $1605. The important thing is that gold managed to hold this level overnight as it closed at 1602. This is on par with a 7 day EMA. Gold is volatile and will react to most economic indicators at its present level, as investors eye the August 1st Fed Reserve meetings.

Crude Oil

Crude Oil (88.47) Crude oil is trading at 88.40 as it seesaws between small gains and losses. Today market has been more focused on news flow then on fundamentals. With little good news, crude oil has little support, but ongoing global tension continues to keep the price off balance against dropping demands and poor eco data. EIA inventories reported an increase in supply.

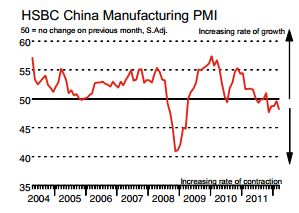

Yesterday’s, EU PMI’s were mostly negative and Chinese PMI reported slightly above expectations but still below the 50 level needed to show growth.