Much of the risk tone facing world markets will be set by the US economy. For the most part this will only happen toward the end of the week not only because US markets are closed for Memorial Day on Monday but also because a series of key reports will be released on Friday that will help determine what kind of momentum the US economy has into the second quarter.

The line-up starts slow with the Conference Board’s consumer confidence index on Tuesday and pending home sales on Wednesday, both of which are expected to be flat.

Consensus expects Q1 US GDP to be revised from 2.2% to 1.9% Thursday partly due to revised trade effects. On that same day, we’ll get a glimpse at the first of the top-tier labor market reports when the ADP private payrolls report arrives. That will be followed by the more complete nonfarm payrolls report and the household survey on Friday.

European markets will pose two main forms of risk to global markets next week. One will be an Irish referendum on the European Fiscal Stability Treaty or the EU fiscal compact on Thursday. Ireland is the only country to hold such a vote within the 25 European nations that signed on to the fiscal pact, as Irish law requires such a referendum to be held on matters affecting sovereignty.

The concern overhanging voters is that Ireland may be cut off from international financial aid if it rejects the treaty, and that is why there is a modest balance of opinion in recent polls that is in favor of a yes vote.

The second main form of European risk comes through key updates on the German economy. Germany’s economy averted recession by expanding 0.5% q/q in Q1 following a small 0.2% decline in Q4. Retail sales are expected to come in flat for the April print, the unemployment rate is expected to hold around a post reunification low of 6.8%, and CPI is expected to be soft enough to justify a further ECB rate cut.

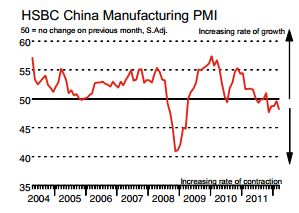

Asian markets will have little capacity to influence the global tone with the possible exception of China’s state version of the purchasing managers’ index that is due out on Thursday night.

Euro Dollar

EURUSD (1.2516) The euro fell below $US1.25 for the first time in nearly two years on concerns that Europe won’t be able to keep Greece in the single currency union.

The euro fell to $1.2518 late on Friday from $1.2525 late on Thursday. The euro fell as low as $1.2495 in morning trading, its lowest level since July 2010. It fell 2 per cent this week and over 5 per cent so far this month.

Traders are concerned that Greece will have to leave the euro if parties opposed to the terms of the country’s financial rescue win an election next month. Those parties were favored in early May, but Greek leaders were unable to form a new government.

The uncertainty could push the euro as low as $1.20 ahead of the June 17 Greek elections, Kathy Lien, director of research at currency trading company GFT said in a note to clients.

The Sterling Pound

GBPUSD (1.5667) Sterling hovered above a two-month low against the dollar on Friday as some investors took profit on earlier bets against the pound, but gains were limited as concerns about a possible Greek euro exit supported demand for the safe-haven U.S. currency.

Expectations the Bank of England may extend its bond-buying programme after the UK economy shrank more than first thought in the first quarter also contained sterling’s rise.

The pound, also called the cable, was 0.05 of a percent higher against the dollar at $1.5680, just above a two-month trough of $1.5639 hit on Thursday.

The euro rose 0.4 percent against the UK currency to 80.32 pence, although it remained within sight of a 3-1/2 year low of 79.50 pence reached earlier this month.

Asian –Pacific Currency

USDJPY (79.68) The JPY is unchanged from yesterday’s close, following the release of mixed CPI data. Japan’s CPI figures have gained importance given the BoJ’s recently announced goal of achieving 1.0% y/y inflation over the next few years, but currently remain short given the recent 0.4% y/y print. The MoF’s Azumi has commented on recent yen strength, but has indicated comfort with current levels given that movement has been driven by risk aversion, and not speculation.

Gold

Gold (1568.90) prices edged higher on Friday after another day of choppy trading but the shiny metal still finished the week lower after broad commodities selling earlier in the week due in part to a strong dollar.

Gold’s globally traded spot contract and New York’s most active futures each rose about 1 percent for the session as investors and traders pared bearish bets ahead of Monday’s Memorial Day holiday, which made for a longer weekend in the United States.

Earlier in the day, gold came under pressure after a plea for help from Spain’s wealthy Catalonia region. That plea forced then euro, already battered by Greece’s woes, to a new 22-month low versus the dollar.

As the session progressed, the precious metal recovered. In Friday’s session, COMEX’s most-active gold futures contract, June, settled at $1,568.90, up 0.7 percent on the day.

On a weekly basis, however, June gold fell 1.2 percent due to losses during the first three days of the week, particularly on Wednesday when almost every commodity plunged.

Spot gold hovered at just under $1,572 an ounce, up 1 percent on the day and down 1.3 percent on the week. In the physical market for gold, buying interest from main consumer India remained light, while gold bar premiums in Hong Kong and Singapore held steady.

Crude Oil

Crude Oil (90.86) prices rose for a second day on Friday on the lack of progress in negotiations with Iran over its disputed nuclear program, but crude futures posted a fourth straight weekly loss as Europe’s debt problems threatened economic growth and petroleum demand.

U.S. July crude edged up 20 cents to settle at $90.86, having moved from $90.20 to $91.32, and remaining inside Thursday’s trading range. For the week, it fell 62 cents and losses during the four-week period total $14.07, or 13.4percent.

Euro-zone political turmoil and economic uncertainty pressured the euro against the dollar, and along with recent signs of slowing Chinese economic growth and rising U.S. crude oil inventories, helped limit gains of Brent and U.S. crude futures.

Iran and world powers agreed to meet again next month to try to ease the long standoff over its nuclear work despite achieving scant progress at talks in Baghdad towards resolving the main sticking points of their dispute.

At its heart is Iran’s insistence on right to enrich uranium and that economic sanction should be lifted before it shelves activities that could lead to its achieving the capability to develop nuclear weapons.