Economic Data for May 10 2012

The calendar has been thin all week; today kicks off with Australia Unemployment numbers and Chinese Manufacturing and Trade Balance and continues to Japan for current account data and trade balance. In Europe, we will see a lot of data coming from the UK including the Bank of England rate decision.

Across to the US we will have unemployment numbers and trade figures.

Euro Dollar

EURUSD (1.2950) The euro is weak, having lost close to 0.2% against the USD, but still trading within yesterdays range. Bond markets are soft, with yields in Italy, Spain, Portugal, France and Greece all moving higher. The break below 1.2955 is disappointing for EUR bulls in an environment where most drivers are turning rapidly bearish. The themes that have supported EUR ytd above levels most would have expected include: repatriation flows, ECB versus Fed policy and the potential for QE3 and finally the value embedded in Germany. We expect the current turmoil to weigh on EUR, but do not expect a collapse and instead look for it to trend towards 1.25 by year‐end.

Headlines are focused on the likely failure of Greece to form a coalition and building expectations that there will be another election on June 10th and that the main issue will be membership within the EMU. This type of uncertainty is likely a EUR negative, even though an eventual exit would be devastating to the people of Greece, but likely positive for EUR. There are other headwinds building, including the May 31 Irish referendum and the upcoming Hollande/Merkel meeting on May 16th followed by the French parliamentary changes.

An escalation of the European crisis is negative for European growth, but as the bottom chart on page 1 highlights it also has negative global growth consequences. On a more positive note, Germany released a wider than expected trade surplus, which rose to €17.4bn and export volumes rose to a new high As such, fears that problems in weaker European countries were leaking into Germany have eased. The French trade deficit narrowed to €‐5.7; however the shift came from of a drop in both exports and imports, suggesting a weakening underlying economy.

The Sterling Pound

GBPUSD (1.6138) Today brings us the policy decision, where the MPC is expected to leave both rates and the asset purchase program unchanged. An elevated inflation profile for the UK is limiting the BoE’s ability to provide easier monetary policy. As such, market participants will have to wait for the BoE minutes release on May 23rd for details about policymakers’ outlook in a deteriorating economic environment GBPUSD continues to decline while EURGBP is flirting with its lows.

Asian –Pacific Currency

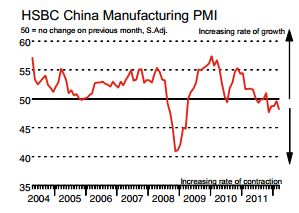

USDJPY (79.69) The yen continues to strengthen as a result of heightened risk aversion, having risen 0.2% from yesterday’s close. Additionally, leading and coincident indicators were stronger, suggesting resilience in the Japanese economy. Just released, trade and current account figures, surprising the markets coming in above forecast. While Chinese data disappointed again.

Gold

Gold (1694.75) Gold slipped today, following a mega rally in the US dollar as global investors eyed the change in French presidency and a selloff in world markets took a toll on the yellow metal. The US dollar rose to its four-month highs against the Euro today, after European voters rejected pro-austerity candidates in weekend elections. Gold had dropped last week and today’s losses meant that a brief bounce after Friday’s non-farm payrolls data proved momentary. French voters elected a new president from the Socialist party, Hollande who plans to turn around the current regime’s focus on austerity in response to Europe’s long-running sovereign debt crisis. Meanwhile, voters in Greece’s parliamentary elections also punished the country’s pro-bailout parties, denying them a majority in parliament.

Crude Oil

Crude Oil (96.81) Nymex crude oil prices declined by 0.7 percent on the back of expected of rise in US crude oil inventories. Additionally, a stronger dollar index and deepening worries over Euro Zone debt crisis also exerted further downside pressure on oil prices. Crude oil touched an intra-day low of $ 96.19/bbl and hovered at $ 96.31/bbl.

The U.S. EIA said in its weekly report that U.S. crude oil inventories rose by 3.7 million barrels in the week ended May 4, above expectations for a 1.97 million barrel increase. U.S. crude supplies rose by 2.84million barrels in the preceding week. Oil prices came off their lows as markets blew a sigh of relief as the government report came after a day after the American Petroleum Institute, an industry group, said that U.S. crude inventories soared by 7.78 million barrels last week. Total U.S. crude oil inventories stood at 379.5 million barrels as of last week, the highest level since August 1980, underscoring fears over a slowdown in oil demand from the U.S.

On the back of increasing worries with respect to Euro Zone debt tensions coupled with weak market sentiments, expect precious energy to trade lower. Additionally, a stronger dollar will also act as a negative factor for prices. Expect crude oil prices to trade with a negative bias on account of the rise in US crude oil inventories along with strength in the US dollar index.