A pair of manufacturing surveys were released today in the US. The Chicago National Activity Index for May showed that conditions had deteriorated somewhat, while the Dallas Fed’s manufacturing survey for June showed an improvement in conditions. After the Philly Fed’s surprising collapse in June, we’ll be watching the other regional Fed surveys especially closely. The Richmond Fed survey for June will be released tomorrow.

US new home sales advanced fairly strongly in May, with the annual rate of sales increasing to 369k from 343k in April, significantly higher than anticipated (the consensus among economists polled by Bloomberg was for an outcome of 346k) . The gains were driven by sales in the Sun Belt. Both median and mean new home prices fell (-0.6% m/m and -3.5% m/m respectively) although both are trending positively in the more medium term at -5% y/y.

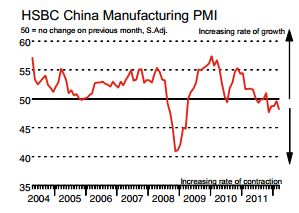

Germany will release consumer confidence data tomorrow along with France. Manufacturing sector surveys from both countries have trended fairly weak for the past two months, so it will be interesting to see how forward looking indicators of consumption are faring. Both surveys will be up to the minute, with the French survey covering the June period while the German survey focuses on expectations for July. Italy will release retail sales data for April as well.

The UK’s budget balance for May will be released, and forecasters polled by Bloomberg are expecting net public sector borrowing of GBP14bn during May. That would put net borrowing at GBP10.7bn for the year.

News flow is expected to pick up as the EU Summit draws near and the Finance Ministers all like getting their own view points out. In a surprise, the newly appointed Greek Finance Minister has resigned after 1 week in office.

Euro Dollar:

EURUSD (1.2507) the pair is bouncing between small gains and losses ahead of the EU Summit, the outlook for the euro is negative. With Spain and Cyprus both summiting official requests for financial assistance. The euro is expected to trade below the 1.24 level. Although no actual results are expected from the EU Summit with investors writing off the outcome, there should be a lot of news.

The Great British Pound

GBPUSD (1.5580) Sterling added a few pips to recover its small losses yesterday on the DX increase of the USD. There was little in the way of eco data on either side of the Atlantic. Today’s give us the UK budget reports.

Asian –Pacific Currency

USDJPY (79.62) In a surprise move, the USD lost some of its momentum against the yen, falling from 80.33, with Japan, dealing with their new tax issues as the government votes today on what is critical for the economy and the yen. The BoJ will respond to the governments outcome.

Gold

Gold (1584.75) is looking for direction once again, ahead of the EU Summit and the end of the month data releases gold continues to bounce between small gains and losses, although it is expected to return to the prior downward trend to 1520 once the EU settles down.

Crude Oil

Crude Oil (79.77) continues to trade on the negative side, as production estimates soar and demand falls, there is at this time a worldwide oversupply of crude. The black gold is expected to remain in this territory for the next 30-60 days barring any political turmoil.